Survey: Why Meeting Small Business Owners Where They are Matters in 2026

Starting a business has always required a certain tolerance for uncertainty. But in 2026, that uncertainty has taken on a new shape. Costs are climbing, trade policy is in flux, and the economic environment is shifting in ways that are difficult to anticipate. And yet, despite it all, most small business owners are still betting on themselves.

That tension between real macro pressure and personal conviction is what Hometap set out to understand in our latest national survey of 1,000 small business owners. In April 2026, we used AYTM to poll both current and aspiring owners of small businesses — defined as businesses with fewer than 100 employees — across generations, genders, and homeownership status to better understand:

- How they're funding their businesses

- What's standing in the way of growth, and

- Where home equity fits into the picture

What we found was a group of people who are clear-eyed about the challenges ahead and determined to push forward anyway. They are largely self-funded, hungry for flexible capital, and navigating a financial landscape that doesn't always work in their favor. But every owner's experience looks very different depending on who you are. Here’s what the data revealed across six key findings.

Finding No. 1: Small business owners are funding themselves

When it comes to financing a business, most small business owners are drawing on what they already have. Personal savings is the most common funding source by a wide margin, with 67% of respondents relying on it. Credit cards follow at 38% and bank loans at 22%. Formal programs like SBA loans (11%) and home equity (7%) barely register.

It’s also worth noting that about 29% of respondents have not yet started their business, meaning this dataset captures aspiring entrepreneurs alongside active operators. For a group this early in the process, the reliance on personal savings over institutional funding isn’t surprising. It does, however, point to a gap between where capital is available and where people actually need it.

Finding No. 2: Economic anxiety is real, but age determines how much it matters

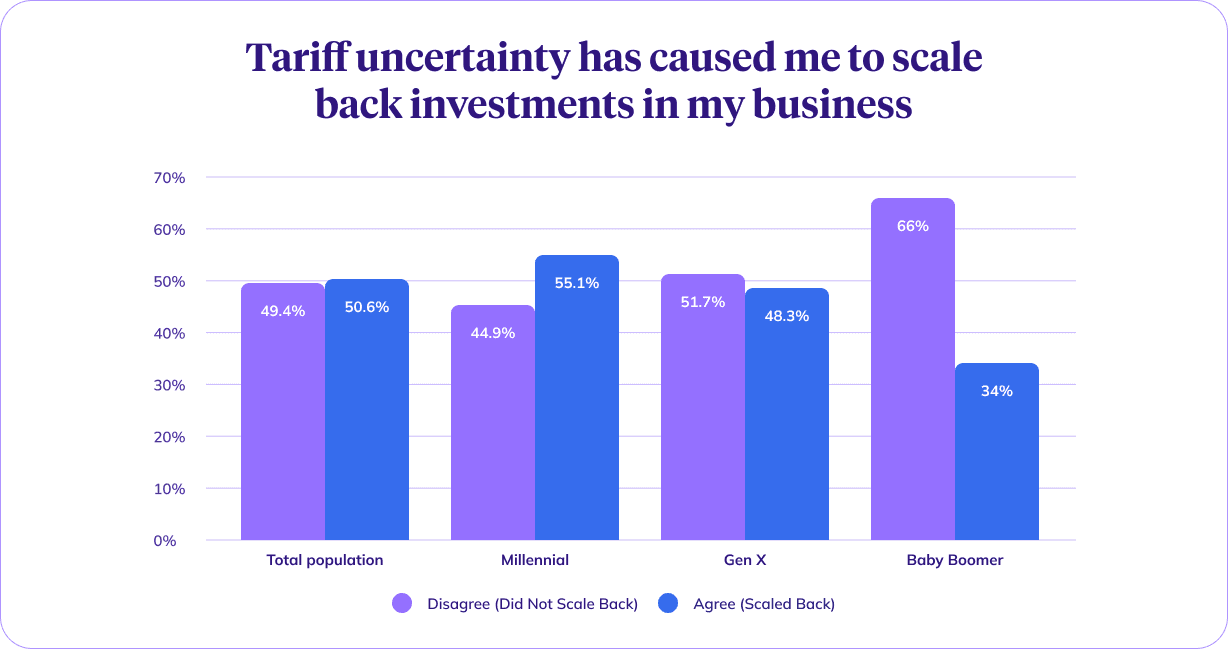

The broader economic environment is weighing on small business owners across the board. 78% say they are concerned about current economic conditions. When it comes to trade policy specifically, the sample divides almost evenly: 51% say tariffs have caused them to scale back investments, while 49% say they have not.

That near-even split, however, obscures a significant generational divide. When asked whether trade policy has caused them to pull back on investments, 55% of millennials say yes, compared to 48% of Gen X and just 34% of baby boomers. The gap reflects something practical: younger business owners have less financial runway to absorb disruption. For millennials, shifting trade policy is a tangible threat to growth plans they’re still building. For boomers, who often have more established businesses and deeper reserves behind them, it largely is not.

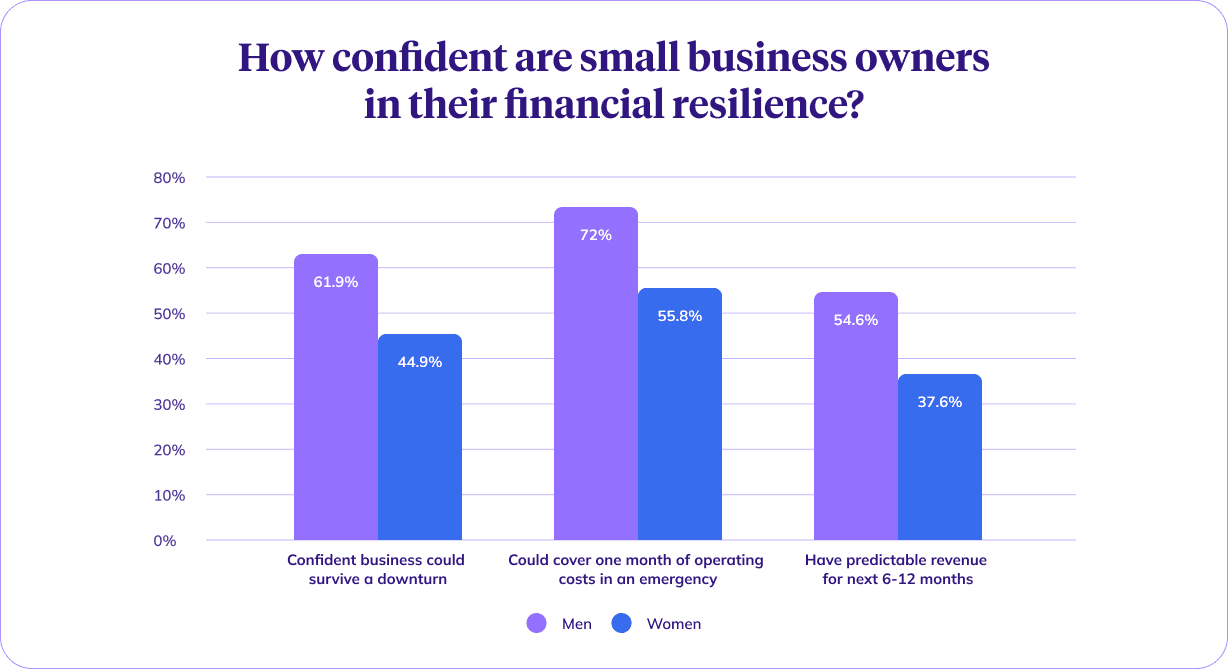

Finding No. 3: Growth expectations are high, but financial resilience is deeply unequal

Despite the macro concerns, 68% of small business owners expect their business to grow in 2026. That optimism is genuine — and it persists even in the face of real economic headwinds. But when you look beyond growth expectations and into financial resilience, the picture becomes considerably more complicated, particularly along gender lines.

Male business owners report substantially higher confidence across every measure of financial stability. For example, nearly 62% of men say their business could survive a downturn, compared to almost 45% of women, and 72% say they could cover one month of operating costs in an emergency, compared to about 56% of women. More than half of men (55%) report predictable revenue for the next 6 to 12 months, compared to over 37% of women. These are not marginal differences, but consistent gaps that point to two meaningfully different experiences of what it feels like to run a small business right now.

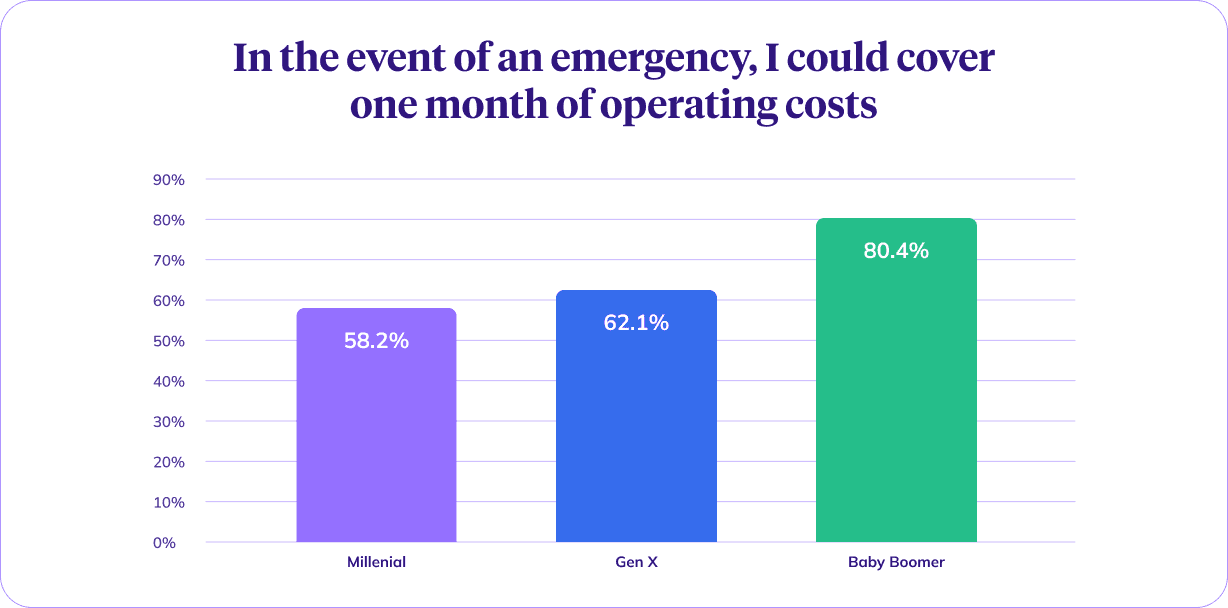

The generational picture adds further texture. Overall, 61% of respondents say they could cover one month of operating costs in an emergency. That figure rises to 80% among boomers and falls to 58% among millennials, with women disproportionately represented among those with the least financial cushion.

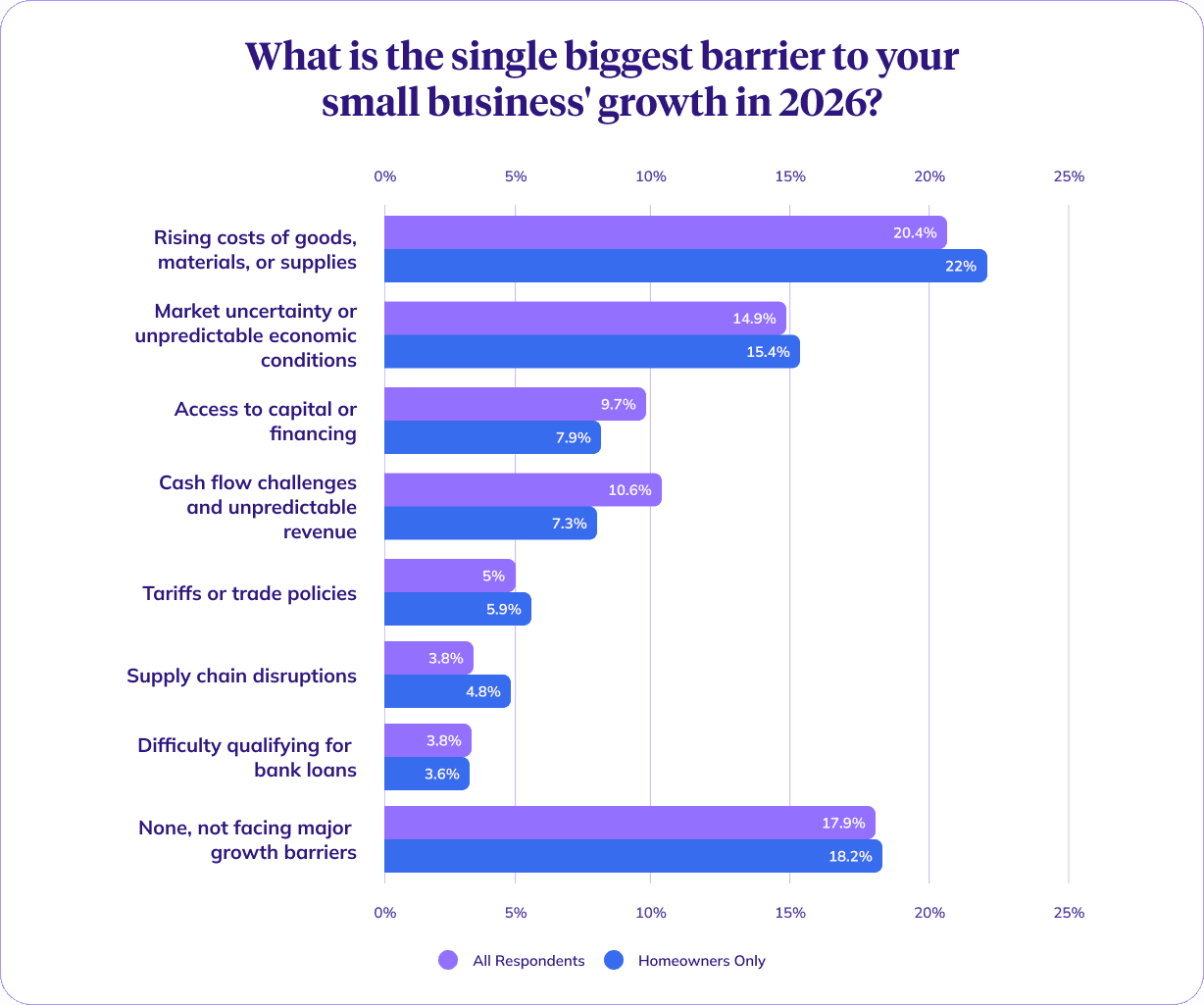

Finding No. 4: Rising costs and market uncertainty are the biggest obstacles to growth

Overall, the rising cost of goods and materials and market uncertainty top the list of barriers to growth, cited by about 20% and 15% of respondents respectively. Among homeowners, the same two barriers lead, though rising costs edge up slightly to 22%, suggesting that owners with more skin in the game feel the squeeze of input costs just a bit more acutely.

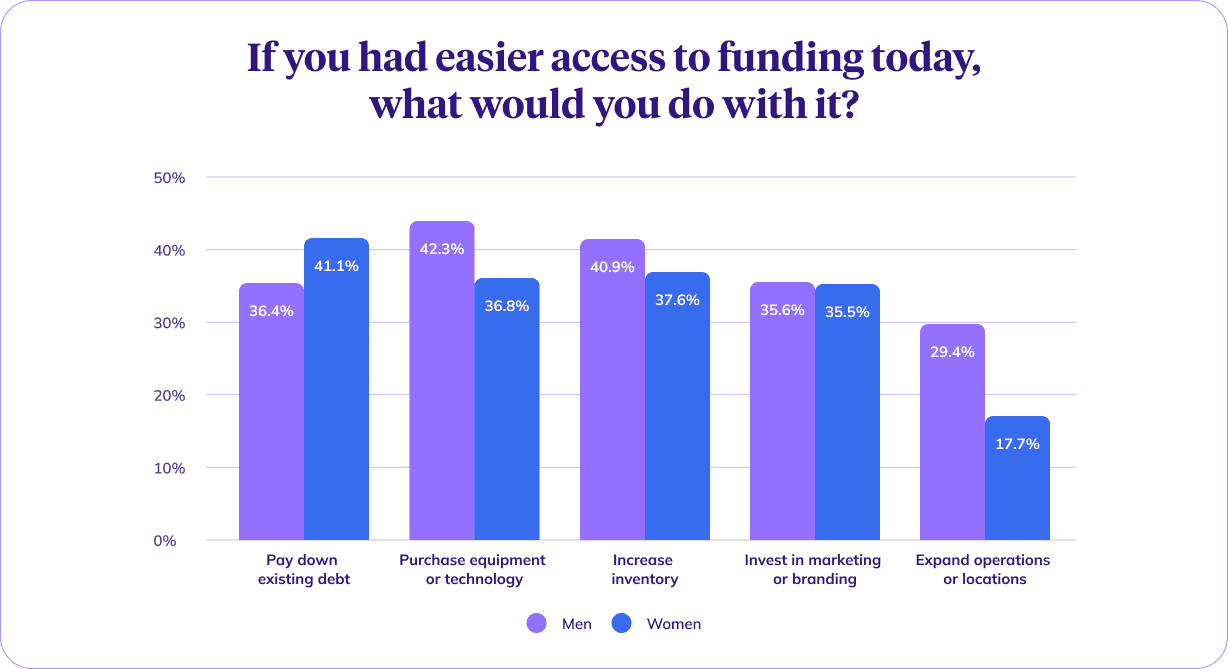

Finding No. 5: More capital would look very different depending on who you ask

If small business owners had easier access to funding, their top priorities would look similar on the surface. The top priorities are paying down debt (39%), purchasing equipment or technology (39%), increasing inventory (39%), and investing in marketing (36%). But the gender breakdown reveals two distinct uses for new capital.

Women prioritized paying down existing debt slightly more than men, at 41% versus 36%. Men leaned more heavily toward expanding operations, at 29% versus 18% for women. Male owners tend to think about new capital as a tool for growth, while female owners are more likely to be focused on stabilizing first. Given the resilience gaps that surfaced in Finding No. 3, that difference likely reflects who is carrying more financial pressure going in, not a difference in ambition.

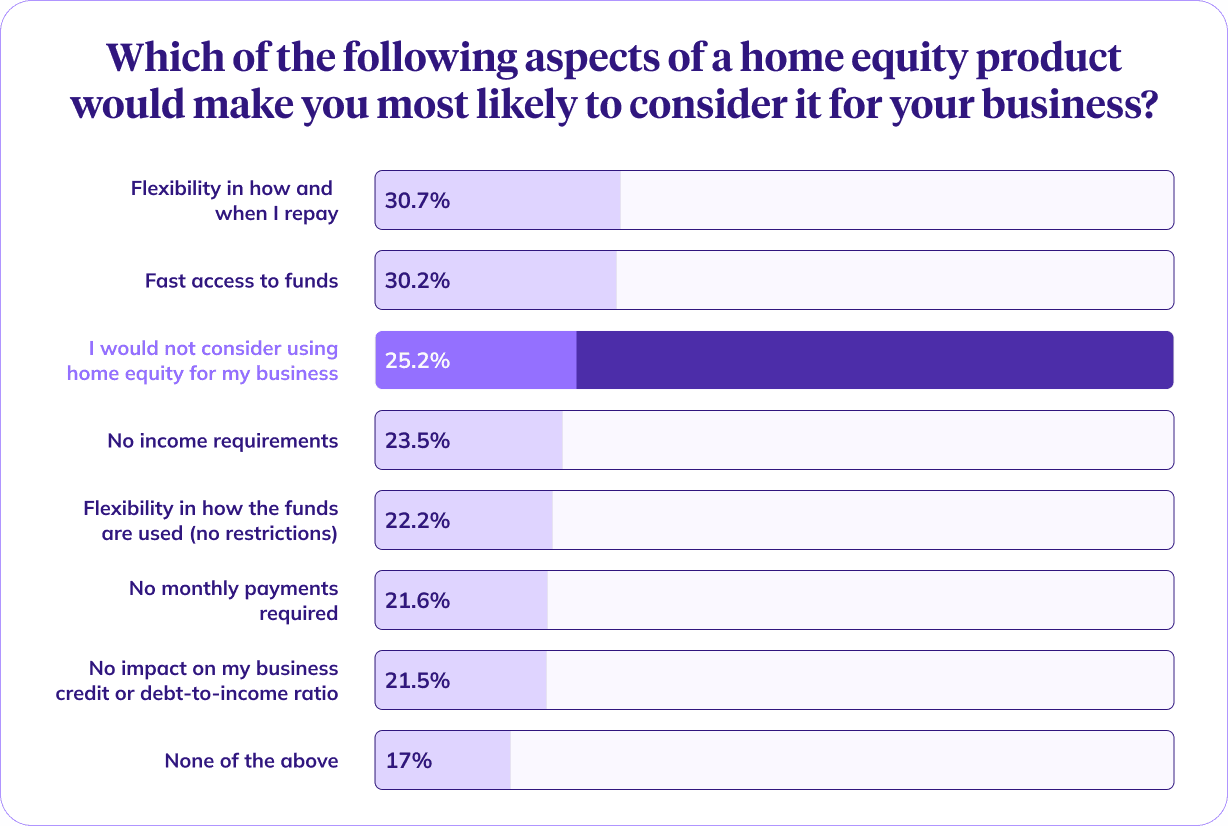

Finding No. 6: Younger owners are the most open to using home equity for their business

When asked what aspects of a home equity product would make them most likely to consider it for their business, flexibility and fast access to funds rose to the top, with each cited by roughly 30% of respondents.

While 25% of respondents said they would not consider using home equity for their business at all — a figure that holds even among homeowners themselves at 26% — that resistance is not evenly distributed across generations.

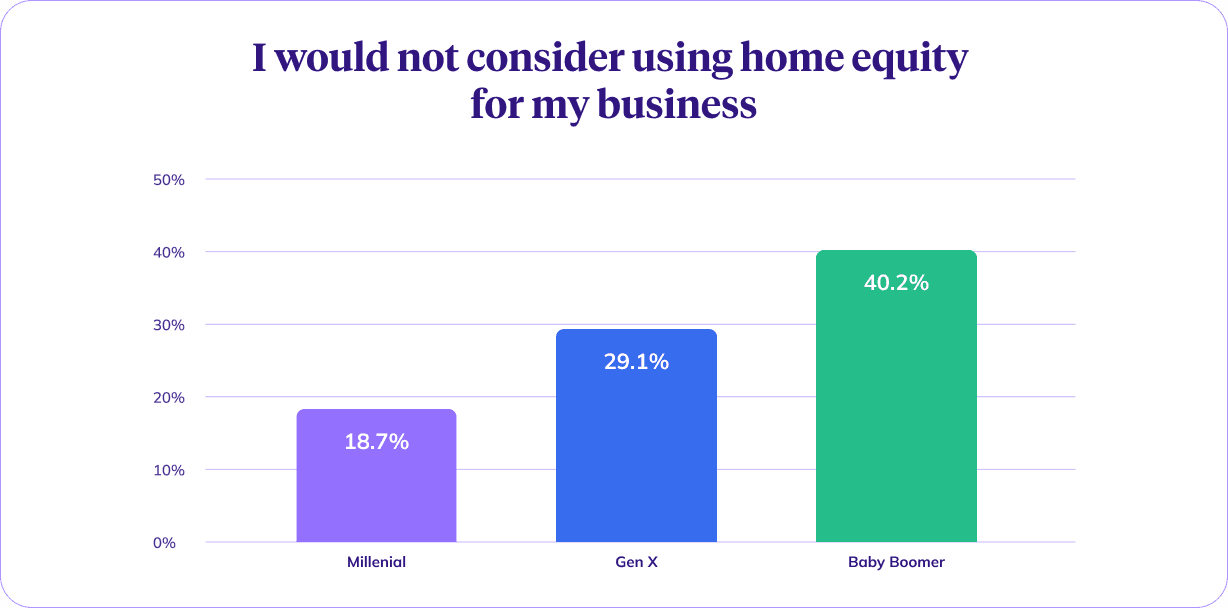

Among millennials, only 19% said they would not consider using home equity for their business, compared to 29% of Gen X and 40% of baby boomers. Younger owners are the most open to putting their home to work for their business. Older owners, despite having the most equity to draw on, are the least likely to consider it for their business.

What small business owners are telling us about capital in 2026

Across generations, the data paints a clear picture. Small business owners are asking for capital that meets them where they are; funding that’s accessible, flexible, and suited to the realities of building a business in an uncertain economy.

And while home equity remains largely untapped as a business funding source, the appetite for these capital solutions is real. Small business owners are ready for financing options that work as hard as they do.

Methodology: The survey was conducted by AYTM on behalf of Hometap from April 14-16, 2026, among 1,000 U.S. small business owners representing a mix of ages, demographics, and regions. Respondents were recruited through AYTM’s online panel and screened to confirm current and aspiring small business owners. The 8-question survey, designed to measure perceptions and sentiments around owning a small business, was administered online with randomized multiple-choice options. The results reflect a 95% confidence level with a ±3% margin of error.

Generations were grouped by the following age ranges: Millennials age 25-44, Generation X age 45-64, and Baby Boomers age 65-79.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.